You’ve finally decided to transform your outdated kitchen or add that desperately needed bathroom, but the estimated $30,000 price tag makes you reconsider. You’re not alone—most homeowners underestimate renovation costs by 20-30%, turning dream projects into financial nightmares. The truth is, learning how to afford a home renovation requires strategic planning, not just deep pockets. Thousands of homeowners successfully complete renovations each year by implementing proven budgeting techniques and creative financing solutions that keep projects on track without draining life savings.

This guide reveals exactly how to afford a home renovation using methods that work in today’s market. Forget the “save until you can pay cash” advice—modern homeowners use smarter approaches that leverage available resources while protecting their financial security. By the end of this article, you’ll know which financing options deliver real value, how to slash costs without compromising quality, and the government programs most contractors won’t tell you about.

Calculate Your Real Renovation Budget Before Spending a Dime

Determine Your True Available Funds

Start with a clear picture of your financial reality by reviewing all accounts without touching emergency reserves or retirement funds. The critical rule experts emphasize: never risk financial security for cosmetic improvements. Calculate your total available cash after preserving 3-6 months of living expenses, then apply the industry standard of 10-20% of your home’s current value as your maximum project cap.

Create a detailed spreadsheet tracking every potential expense—materials, labor, permits, design fees, and often-overlooked costs like temporary housing or takeout meals when your kitchen’s unusable. Professional contractors consistently report that homeowners who document expenses upfront stay 23% closer to their original budget than those who don’t.

Build an Unbreakable Contingency Fund

Every successful renovation includes a 15-20% safety net for the inevitable surprises—hidden water damage, outdated wiring, or permit complications. Document potential cost triggers before demolition begins, including storage fees for furniture and utility bill increases during construction. This proactive approach prevents budget blowouts when contractors discover rotted subfloors or outdated electrical systems behind walls.

Track your contingency spending separately from your main budget to maintain clear visibility. When unexpected issues arise (and they will), this dedicated fund keeps your project moving without derailing your entire financial plan or forcing you to abandon half-finished work.

Financing Options That Actually Make Renovations Affordable

Traditional Financing Routes Worth Considering

Cash Savings: While paying cash eliminates interest and often secures 5-10% contractor discounts, it dangerously depletes your financial safety net. Reserve this approach for projects under 5% of your liquid assets—anything larger risks your emergency fund.

Home Equity Loans: These fixed-rate second mortgages provide lump sums at 2-6% interest with predictable payments. Borrow up to 85% of your home’s value minus existing mortgage balance, ideal for major renovations requiring substantial upfront capital.

HELOC Flexibility: Home Equity Lines of Credit function like credit cards secured by your property. Access funds as needed during phased renovations while paying interest only on amounts used, with most offering 5-10 year draw periods perfect for multi-stage projects.

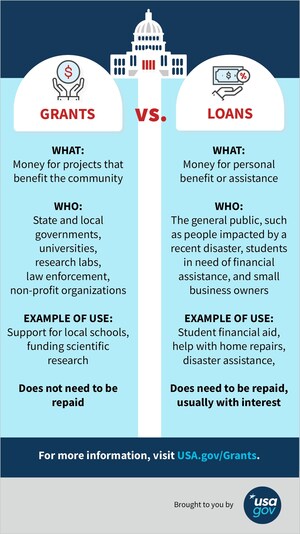

Government-Backed Renovation Loans You Qualify For

FHA 203(k) Programs: These specialized mortgages combine purchase or refinance with renovation costs into one loan. The standard version handles major projects over $35,000, while limited 203(k) covers smaller improvements under $35,000—both requiring licensed contractors but offering significant savings over separate financing.

Fannie Mae HomeStyle: More flexible than FHA options, these conventional loans allow luxury upgrades and landscaping while borrowing up to 75% of your home’s post-renovation value. Perfect for substantial improvements that significantly increase property worth without immediate cash outlay.

Utility Company Programs: Many providers offer 0% financing for energy-efficient improvements like windows, insulation, or HVAC systems. Repay through monthly utility bills with savings often covering the payment—effectively making these upgrades free while lowering long-term costs.

Slash Renovation Costs Without Sacrificing Quality

Implement Strategic Phased Renovations

Break major projects into 2-5 year timelines aligned with tax refunds, bonuses, or seasonal contractor discounts. Start with structural necessities—roof, electrical, plumbing—before cosmetic updates to maximize safety and functionality per dollar spent.

Schedule labor-intensive phases during contractors’ slow seasons (typically January-March) for potential 15-20% discounts. One homeowner saved $8,500 by completing bathroom renovations in February instead of summer peak season, proving timing significantly impacts how to afford a home renovation.

Master Material Cost Reduction Tactics

Smart Sourcing Strategies: Purchase flooring, fixtures, and appliances during late fall clearance sales when contractors reduce inventory. Establish relationships with local suppliers for contractor pricing—even DIY purchases can qualify for professional discounts with the right approach.

Salvage Yard Secrets: Architectural salvage yards offer vintage doors, fixtures, and lumber at 50-80% below retail. These materials often exceed modern quality while adding unique character—just verify compatibility with current building codes before purchasing.

Factory Seconds Advantage: Ask suppliers about overstock or discontinued products. Premium tile, cabinetry, and fixtures frequently sell at 30-60% discounts simply because they’re last season’s models, freeing up budget for higher-impact elements.

Contractor Negotiation Tactics That Save Thousands

Never accept the first quote—obtain 3-5 detailed bids specifying exact materials and timelines. Research credentials through state licensing boards and verify insurance coverage including $1 million general liability and workers’ compensation.

Negotiate payment schedules tied to verified completion milestones rather than calendar dates. Never pay more than 10% upfront, and offer scheduling flexibility during contractors’ slower periods for potential discounts. One homeowner secured 12% off her kitchen remodel by allowing the contractor to schedule cabinetry installation during a two-week gap between larger projects.

Government Programs That Slash Your Renovation Costs

Federal Assistance You’re Eligible For

HUD Title I Loans: These insured loans provide up to $25,000 for home improvements without equity requirements. Use them for essential upgrades like roofing or plumbing with competitive interest rates due to federal backing—perfect when you need to know how to afford a home renovation with limited savings.

Energy Tax Credits: Federal programs cover 30% of costs for qualifying energy-efficient improvements including windows, doors, and insulation. These credits directly reduce your tax liability dollar-for-dollar, effectively making certain upgrades almost free.

State and Utility Company Programs

Weatherization Assistance: State-administered programs provide free energy efficiency upgrades for qualifying households. Services include insulation, weatherstripping, and HVAC improvements that reduce utility bills long-term—check eligibility through your state housing agency.

Utility Rebates: Major providers offer $50-$1,500 rebates for energy-efficient appliance upgrades. Some even provide 0% financing with repayment through monthly bills, making these improvements cash-flow positive from day one.

Protect Your Budget During Construction

Implement Bulletproof Payment Schedules

Structure contractor payments around verified completion milestones: 10% at signing, 25% after material delivery, 25% at rough-in completion, 25% after substantial completion, and 15% final payment. Use escrow accounts for projects exceeding $50,000 to ensure funds release only after satisfactory inspections.

Create a separate checking account exclusively for renovation expenses—this simplifies tracking, prevents budget confusion, and provides clear documentation for potential tax benefits. Reconcile expenses weekly against your original budget to catch variances early.

Track Every Dollar Like a Professional

Document receipts immediately with digital photos stored in cloud-based folders. Categorize expenses by room, phase, and material type using renovation-specific software or detailed spreadsheets. One homeowner caught a $2,000 material overcharge before installation began simply by tracking expenses weekly.

Establish secondary funding sources before demolition starts—pre-approved credit lines or alternative financing options provide safety nets when hidden issues emerge. Budget 10-15% additional time beyond contractor estimates to avoid costly rush fees when delays occur.

Maximize Your Renovation’s Long-Term Value

Focus spending on high-return projects like garage door replacements, manufactured stone veneers, or minor kitchen remodels that deliver 75-100% ROI in most markets. Avoid over-improving beyond neighborhood standards—your $50,000 kitchen won’t recoup costs in a $250,000 home.

Calculate payback periods for energy-efficient upgrades—insulation, HVAC, and window projects often achieve full payback within 5-10 years through utility savings alone. Update homeowner’s insurance immediately after renovations to protect your investment, and budget 1-3% annually for maintenance to prevent small issues from becoming expensive problems.

The homeowners who successfully figure out how to afford a home renovation start with realistic budgeting, explore every financing option, and implement cost-cutting strategies that maintain quality. Remember: the cheapest option isn’t always most affordable long-term. Invest in quality where it matters—structural elements, electrical systems, and plumbing—while saving on cosmetic features you can upgrade later. With these proven strategies, you’ll transform your space while keeping your financial future secure. Start by downloading a renovation budget template today—your dream home renovation is closer than you think.